The ETC’s quarterly report analyses the performance, trends and outlook for European tourism during the first half of 2026, comparing these with the performance for the same period in the previous year. Overall, the year got off to a good start with an increase in tourism demand in Europe, reinforcing its role as the world’s leading destination, despite a global context marked by climate risks and international economic and geopolitical uncertainties.

In the first half of 2026, international arrivals in Europe rose by 5% compared with 2025, and overnight stays increased by 4.8%. In most European destinations, average spending per visitor also rose, reflecting consumers’ willingness to continue travelling even at higher costs, prioritising leisure and cultural discovery.

The report focuses on four key areas: tourism and economic performance in the first half of 2026; the outlook for international tourism; recent performance of the industry; and the performance of the most significant source markets.

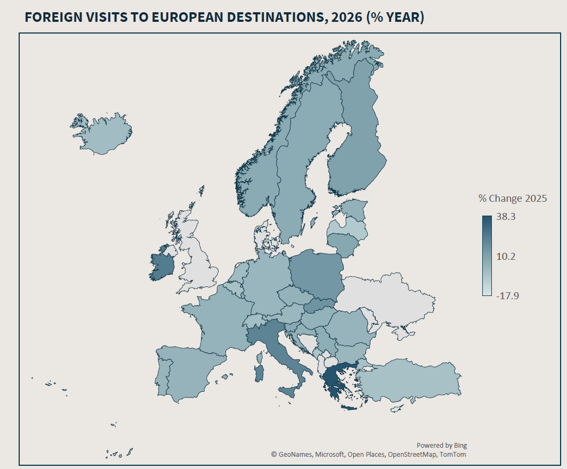

European tourism demand ended the first half of 2026 with a 5 per cent increase in international tourist arrivals compared with the same period the previous year. The vast majority of European destinations recorded growth in arrivals compared with 2025. Greece (+38%), Italy (+21%) and Malta (+16%) performed strongly, driven by intercontinental demand.

Figures for the first half of 2026 show that international tourist arrivals in Europe rose by 5 per cent compared with the same period in 2025. Northern Europe was the best-performing sub-region compared with the previous year, with an increase in arrivals of around 10 per cent, against an 8.4 per cent rise in overnight stays. This was followed by the Mediterranean region, where the increase in overnight stays was slightly higher than the number of arrivals, indicating a trend towards longer stays. Poland led the performance of Central European countries, driving a 5.2 per cent increase in arrivals and a 6.9 per cent increase in overnight stays for the sub-region.

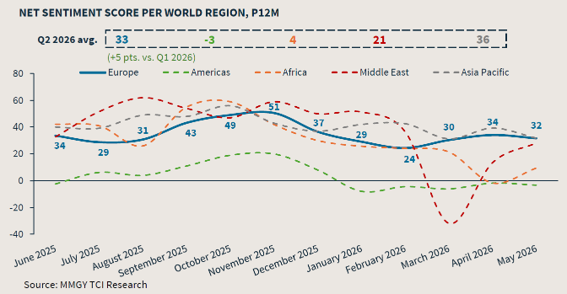

Another aspect analysed was online sentiment regarding travel within Europe, which peaked at 34 points in the second quarter of 2026, representing a year-on-year increase of 5% compared with the first quarter of 2025. Despite the ongoing conflict in the Middle East and growing uncertainty about its impact on global aviation fuel costs, optimism rose slightly in April 2026. Discussions about rail travel, including new routes and European initiatives to improve access for young travellers, provided a positive counterbalance. May saw a slight decline, driven in part by extreme weather events at the start of the season. Nevertheless, Europe retained second place globally in terms of optimism in the second quarter, just behind the Asia-Pacific region.

Demand for air travel in Europe was on an upward trend at the start of 2026, with strong growth in demand, measured in revenue passenger-kilometres (RPK), recording a 7.0 per cent increase in the first quarter, with March being the best-performing month of the quarter (up 8.0 per cent).

The average load factor in the first quarter of 2026 was 79.0 per cent, an increase of 1.6 percentage points compared with the first quarter of 2025. Strong growth in demand drove the load factor in March up to 81.3 per cent, compared with 78.0 per cent in the previous year. Service disruptions and flight cancellations linked to the conflict in the Middle East reduced capacity, thereby raising the load factor. The ongoing impacts of the conflict persisted in April, when demand fell and RPK growth stood at 0.9%.

Air capacity (the number of available seats) grew at a markedly slower pace in April, rising by just +0.4 per cent, reflecting capacity cuts by airlines at a time of lower demand. Nevertheless, the load factor rose to 84.9 per cent, largely in line with previous years, as the reduction in capacity helped to offset weaker traffic. These cuts are putting pressure on airlines, which have to cope with diverted flights and higher fuel costs. If capacity growth remains weak during the peak summer season, the load factor is likely to rise further, as demand is forecast to grow.

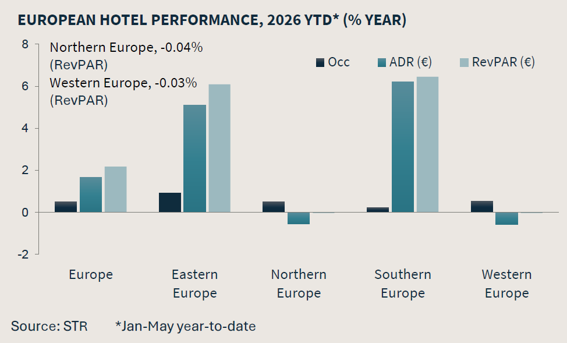

As regards accommodation, Europe performed well in early 2026, with RevPAR growing by 2.2 per cent, supported by a 0.5 per cent rise in occupancy rates and a 1.7 per cent increase in ADR. The strongest gains were recorded in southern European countries, with significant increases in RevPAR and ADR of around 6 per cent, driven by strong intra-continental demand and also benefiting from the impact of the Winter Olympics. By contrast, the gains seen in Western and Eastern Europe were driven by demand for more budget-friendly accommodation categories.

The supply of short-term rental properties (short-stay accommodation) in Europe reached 5.4 million units in May 2026, an increase of 3.0 per cent compared with the previous year. The supply of this type of accommodation in Europe grew in both April (+2.2% year-on-year) and May 2026 (+3.0% year-on-year). The average gross daily rate across Europe rose by an average of 13.3% year-on-year between April and May, with monthly rates recording a year-on-year increase of 12.0% in April and 14.5% in May. In both months, increases in the average daily rate outpaced growth in supply, with both metrics showing a year-on-year increase.

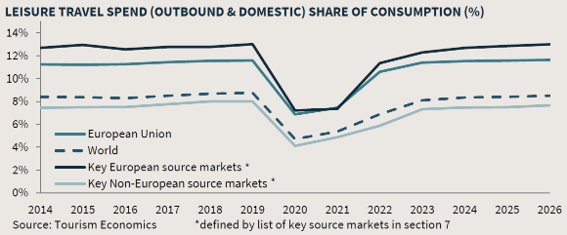

As the 2026 summer season gets underway, the outlook for the performance of the tourism sector remains optimistic. Leisure travel is expected to remain a priority for consumers ahead of the summer period (July to August), despite ongoing economic uncertainty and persistent pressures on affordability. In the main European source markets, spending on leisure travel is forecast to remain stable at 13.0 per cent of total consumer spending in 2026, well above the global average of 8.5 per cent. In the main non-European source markets, this share is forecast to rise slightly to 7.7 per cent, up from 7.5 per cent in 2025.

These forecasts show that consumers still prioritise travel experiences, but are becoming more selective about where and how they spend their money. As a result, destinations that align most closely with travellers’ budgets and preferences are likely to be better placed to attract demand in the coming months.

European travellers will increasingly favour destinations closer to home. European destinations are likely to continue to benefit from strong intra-European travel flows. For many travellers, destinations closer to home are more familiar, easier to reach and offer greater flexibility. They may also offer better value for money, as cost considerations become increasingly important.

European travellers are showing increasing price sensitivity. In the latest Travel Industry Monitor survey, 48 per cent of European respondents identified affordability and value for money as a key opportunity for Europe in the second quarter, up from 32 per cent in the first quarter.

Southern and Mediterranean destinations are well placed to capture demand for intra-European leisure travel. The latest ETC barometer indicates that interest in Southern and Mediterranean Europe between June and November rose to 61% (+4%), further reinforcing the region’s strong appeal.

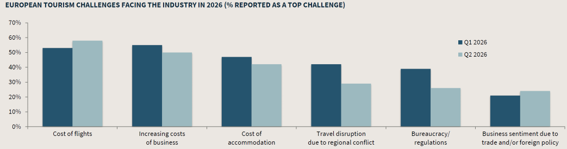

The results of the Travel Industry Monitor for the second quarter of 2026 show that the cost of airfares has become the main concern for industry experts, as disruptions to supply chains in the Strait of Hormuz continue to put pressure on energy and aviation fuel prices. This has further increased pressure on airfares and flight capacity in Europe.

Travel disruptions linked to the conflict in the Middle East remain a major challenge, but sentiment in Europe is less negative than global sentiment.

Although fewer European respondents highlighted the cost of doing business as a key challenge in the second quarter compared with the first-quarter survey, the European tourism sector continues to face rising costs for energy, labour and supplies. As businesses pass these higher costs on to consumers, this will drive up prices, putting pressure on both households and businesses this year.