The quarterly report by the European Travel Commission (ETC) analyzes the performance, trends, and outlook of European tourism during 2025 and the first quarter of 2026. Overall, the year started positively, with increased tourism demand in Europe reinforcing its position as the world’s leading destination, despite a global context marked by climate risks and international economic and geopolitical uncertainties.

In 2025, international arrivals to Europe increased by 3.5% compared to 2024, while overnight stays grew by 3.3%. In most European destinations, average spending per visitor also rose, reflecting consumers’ willingness to continue traveling despite higher costs, prioritizing leisure and cultural discovery.

The report focuses on four key areas: tourism and economic performance in 2025 and Q1 2026; outlook for international tourism; recent industry performance; and performance of the most relevant source markets.

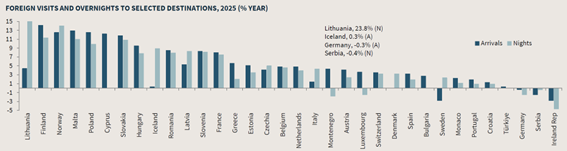

European tourism demand closed 2025 with a 3.5% increase in international tourist arrivals compared to the previous year. Nearly 90% of European destinations recorded growth in arrivals compared to 2024. France (+8%) and Spain (+3%) showed strong performance, accompanied by increased visitor spending.

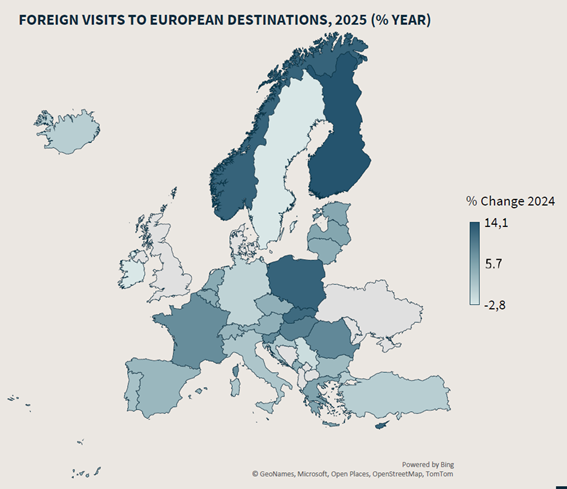

Data for the first quarter of 2026 show that international tourist arrivals to Europe increased by 5.6% compared to the same period in 2025. Ireland (+30%) and Finland (+12%) stood out in Northern Europe. Strong gains were also observed in ski destinations, including Italy (+14%), Austria (+7%), France (+5%), and Switzerland (+3%), all showing steady growth. Italy received an additional boost from the Milan-Cortina 2026 Winter Olympic Games.

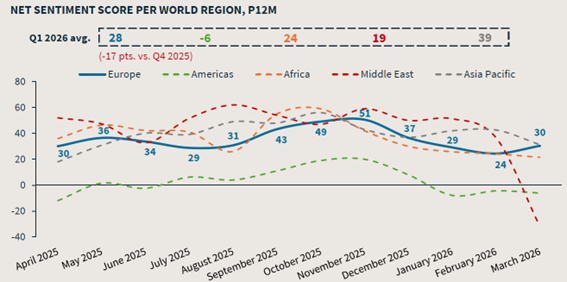

Another aspect analyzed was online sentiment regarding travel in Europe, which stood at 28 points in the first quarter of 2026, a drop of 17 points compared to the fourth quarter of 2025. This decline from December 2025 extended into January, driven by several negative news stories related to incidents during New Year celebrations. In February, sentiment was further impacted by controversy surrounding the Winter Olympics in Italy, as well as the escalation of the conflict in the Middle East and the resulting travel disruptions, which left many Europeans stranded and continue to affect long-haul travel dependent on regional routes.

Travel demand in Europe ended 2025 on a high note, with the revenue passenger kilometers (RPK) indicator rising by 7.4% in the fourth quarter, the best-performing quarter of the year. Early 2026 data show that growth momentum continues, with travel demand increasing by 6.8% and 5.6% in January and February, respectively, compared to the same months in 2025.

The load factor averaged 83.9% in 2025 (in line with 83.8% in 2024), reaching a peak of 86.6% in December. In line with seasonal trends, occupancy rates declined at the start of 2026. February recorded a load factor of 76%, 0.8 percentage points higher than February 2025. Although the load factor increased this year, it remains below the 2019 peak (82.4%) as supply growth outpaced demand during this period.

Regarding accommodation, Europe showed strong performance at the start of 2026, with RevPAR growing by 2.3%, supported by a 0.9% increase in occupancy rates and a 1.4% rise in ADR. Midscale and upscale segments recorded growth, reinforcing the idea that travelers continue to prioritize stays offering good value for money and/or high quality outside peak periods.

The supply of short-term rental properties (local accommodation) in Europe reached 5.1 million units in March 2026, an increase of 0.8% year-on-year. This represents a sharp slowdown compared to the 5.1% recorded in February, due to the seasonal reduction in property listings and regulatory pressures in several key markets. After a 2.1% year-on-year decline in Q4 2025, the average daily rate (ADR) for short-term rentals showed a strong recovery in Q1 2026, increasing by 11.4%, suggesting that the stabilization of supply growth may be supporting higher prices.

The ongoing instability in the Middle East has negatively impacted global tourism flows, particularly intercontinental traffic that relies on regional air hubs as key connection points between Europe, Asia, and Africa. Nevertheless, Europe is expected to benefit the most from increased regional travel, as tourists postpone or redirect trips that would otherwise have been to the Middle East and further eastern regions. This substitution is expected to sustain demand within Europe throughout the year.

In fact, Europe is less vulnerable than Africa and Asia-Pacific because around 80% of international travel is intra-regional, limiting the proportion of overnight stays at risk. A strong base of regional demand helps cushion the impact of long-haul travel disruptions. Moreover, during periods of instability in the Middle East, European travelers tend to choose destinations perceived as safer and further from the conflict.

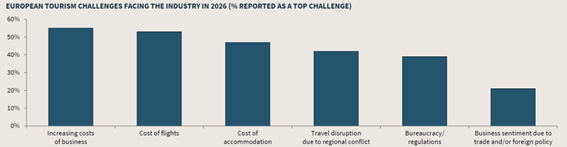

It is also worth noting the latest results from the “Travel Industry Monitor” survey for Q1 2026, which show that a growing number of professionals identify flight costs as a key challenge for 2026. This aligns with the rise in global energy prices in March, following the conflict involving the United States, Israel, and Iran. Respondents expect airlines to pass higher costs on to consumers.

Rising energy costs will increase operating expenses across the entire sector, including accommodation. Prices are not expected to reach the peaks of 2022, but they remain high compared to historical standards, and consumers are seeking better value for money. The recent temporary increase in prices adds further pressure on European establishments.

Travel disruption and displacement due to regional conflicts were added as a new challenge in the Q1 survey, reflecting the ongoing conflict in the Middle East. Among respondents, 42% identified this as a key challenge; 55% expect weaker inbound tourism, compared to 16% who expect stronger international demand. The main source of optimism is the expectation of increased domestic tourism (34%), driven by the shift of some international trips to domestic markets.