This report aims to provide an in-depth analysis of the hostel sector in Portugal between 2022 and 2025, including a detailed comparison of the 15 most significant municipalities. It analyses temporal, quantitative and territorial trends, focusing on tourist concentration and regional differences.

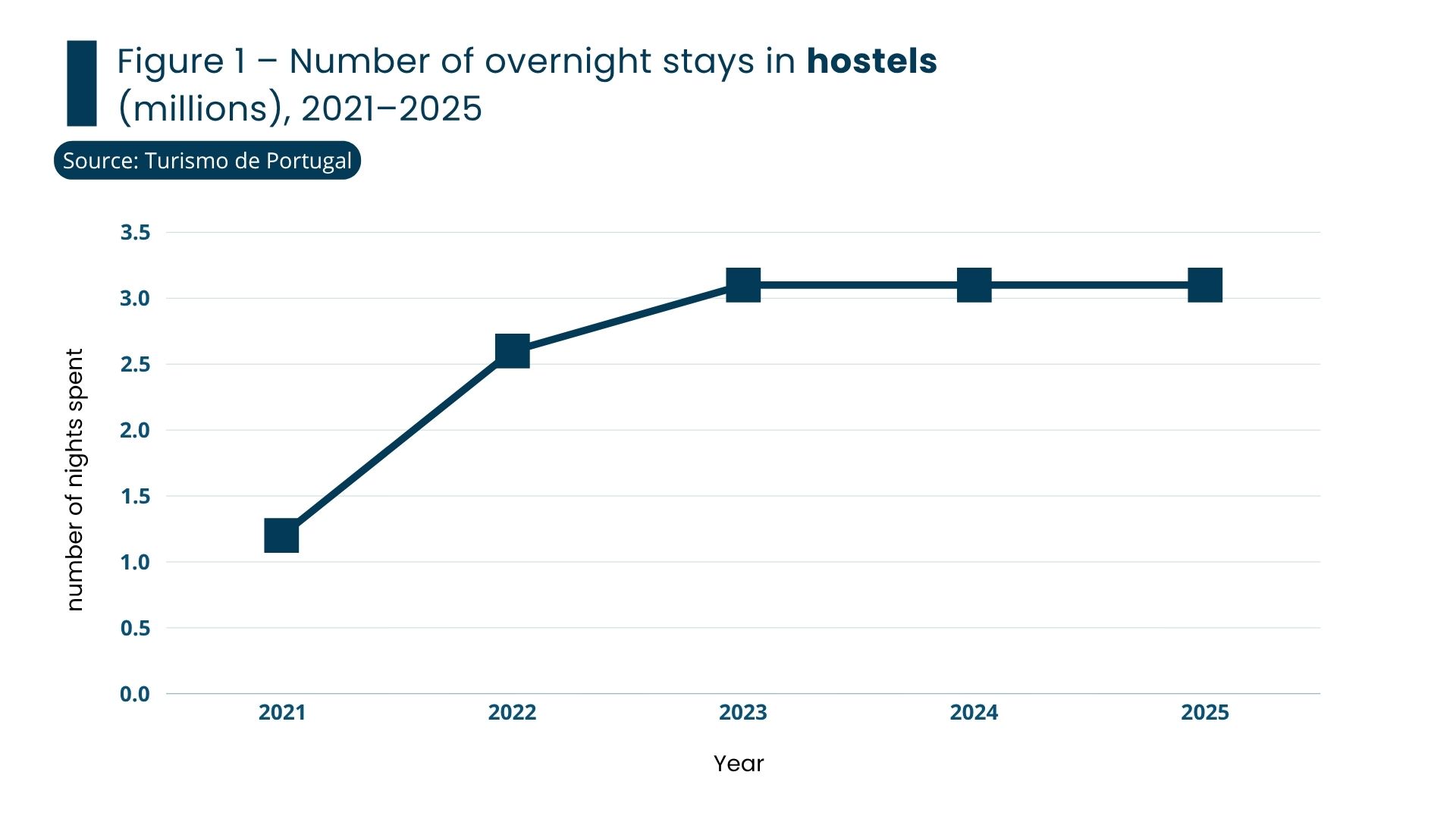

Between 2022 and 2025, the sector went through three phases: recovery (2022), growth (2023–2024) and stabilisation (2025). Demand increased significantly following the pandemic, followed by a recent slowdown. Overnight stays rose from around 2.7 million in 2022 to over 3.1 million in 2024, stabilising in 2025. The average length of stay decreased, reflecting the growing importance of short stays.

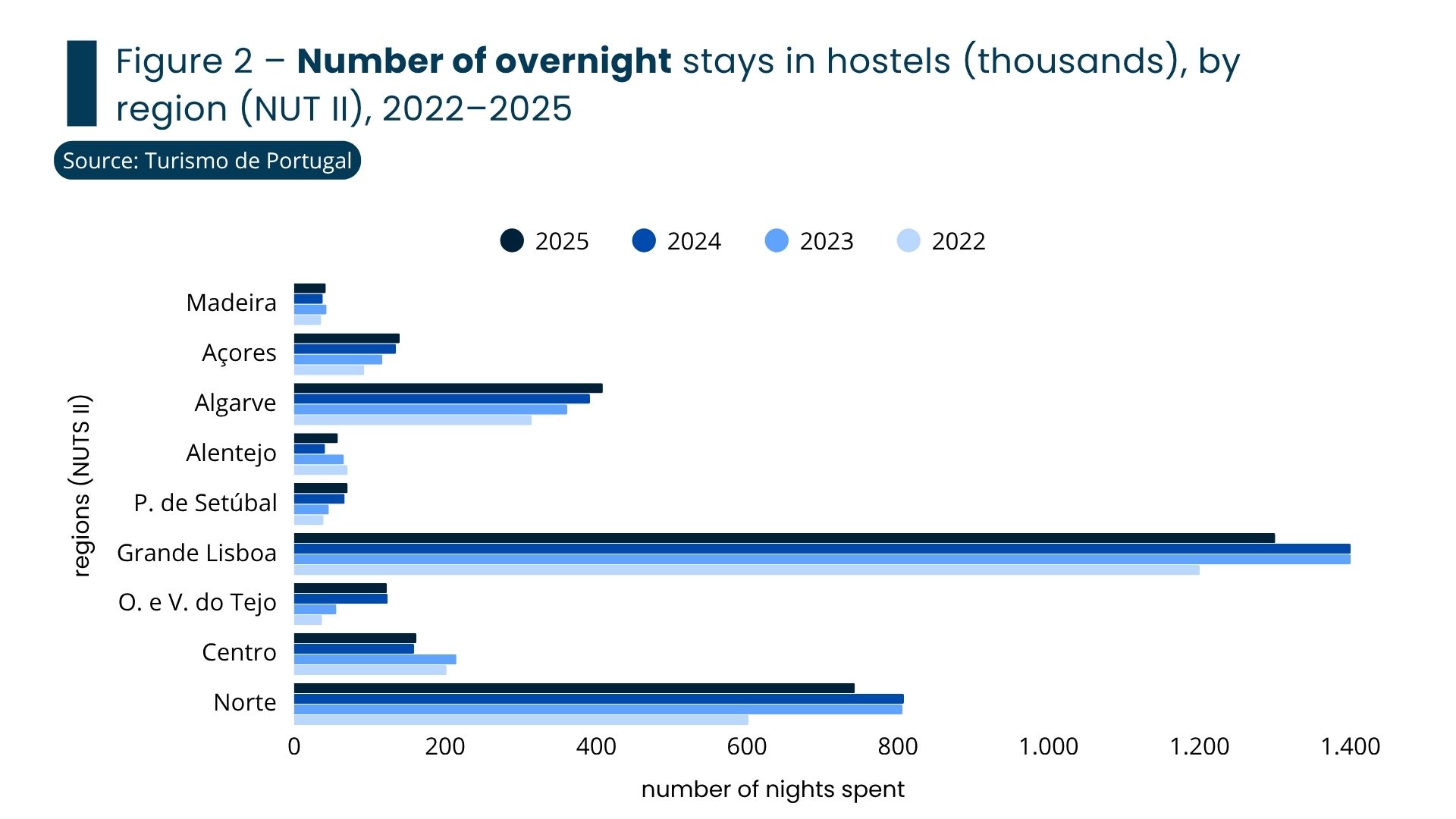

Lisbon and Porto clearly stand out as the main tourist hubs, accounting for the majority of overnight stays. The Algarve has a high level of tourist activity, whilst the remaining municipalities show regional significance or emerging growth.

Comparison by year (2022–2025)

2022: Strong concentration in Lisbon and Porto. This year marks the post-pandemic recovery point and is essential for interpreting subsequent developments: overnight stays: 2.6 million; growth: +118% compared with 2021; accommodation supply: 435 hostels and just over 18,000 beds; geographical concentration in Lisbon and Porto, which accounted for around 55% of demand.

Key trends for 2022: A strong ‘rebound’ effect (abrupt recovery); increased importance of urban destinations, particularly Lisbon.

2023 and 2024: Expansion into the Algarve and the islands, and consolidation of secondary destinations. Over these two years, the available data show strong growth on both the supply and demand sides, against a backdrop of significant acceleration in all tourism activity. Cumulative change (2023 and 2024) in the main hostel indicators: number of establishments, +20%; capacity, +19%; overnight stays, +19%; guests, +17%; total revenue, +32%.

Key trends for 2023–2024: Transition from a recovery phase to one of sustained growth; a stronger increase in revenue than in demand, with price rises reflecting the product’s increased value. Hostels have benefited from increased demand from young international travellers and from the search for more affordable accommodation options.

2025: Stabilisation of demand and supply, and relative growth in medium-sized cities. There is a sharp slowdown on both the supply and demand sides, reflected in reduced growth rates: number of establishments, +1.9 per cent; capacity, +6 per cent; overnight stays, -2.2 per cent; guests, -1.5 per cent; total revenue, -1.5 per cent.

Key features of 2025: much more moderate growth, entering what might be described as a possible phase of maturity. The decline, albeit slight, in overnight stays compared to the number of guests indicates shorter stays and higher turnover in accommodation occupancy.

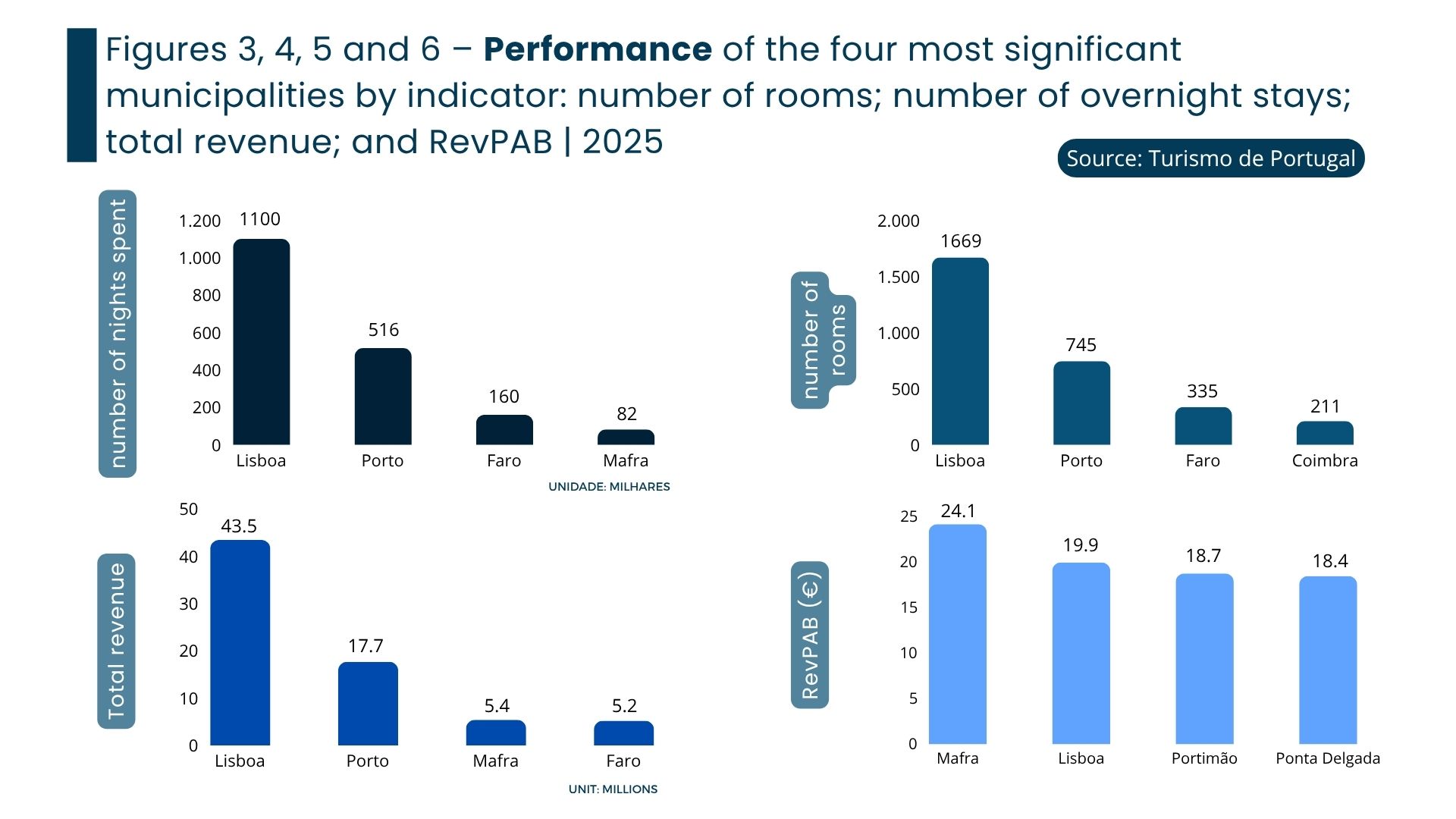

Lisbon stands out for having the widest range of accommodation and the greatest diversity of demand. Porto has seen strong growth in recent years. Albufeira and Loulé lead the way in terms of tourist numbers. In the autonomous regions, Funchal and Ponta Delgada stand out as leading destinations. Some district capitals, such as Braga, Coimbra and Aveiro, are showing sustained growth.

The 15 most significant municipalities are: Lisbon, Porto, Albufeira, Loulé, Portimão, Lagos, Faro, Cascais, Sintra, Vila Nova de Gaia, Funchal, Ponta Delgada, Braga, Coimbra and Aveiro. Nevertheless, these can be divided into three distinct groups, taking into account the different levels of supply and demand. The first group comprises the most significant municipalities: Lisbon, Porto, Albufeira, Loulé and Funchal. An intermediate group, of medium significance, includes: Cascais, Lagos, Portimão, Sintra and Vila Nova de Gaia. The final group, of lesser significance, comprises: Faro, Ponta Delgada, Braga, Coimbra and Aveiro.

Conclusion

The results show a high degree of geographical concentration, albeit with signs of gradual territorial diversification. The pressure exerted by tourism on the main urban centres poses a significant challenge to the sector’s sustainability.

It is also evident that the sector is becoming increasingly mature, with significant regional differences. Despite the clear dominance of Lisbon and Porto, other municipalities have been increasing their importance, with future development heavily dependent on the ability to promote a greater territorial spread of demand.

Overall, the sector has evolved from quantitative growth to a more mature model focused on value creation, with recent signs of adjustment in demand. Among the main challenges facing the sector in the near future, the following stand out:

reducing seasonality and urban pressure (Lisbon and Porto);

identifying possible changes in tourist behaviour;

countering the trend towards shorter stays;

responding positively to increased price sensitivity.